Can you get a business credit card with no personal guarantee?

Running a business is a stressful pursuit, especially if you have to put up a personal guarantee to get your business credit card. When you personally guarantee your company's credit card debt, you’re responsible for repaying it if your business can’t.

That’s what makes business credit cards with no personal guarantee so attractive: The business, not the owner, is responsible for all debts. This creates a clear financial separation between your company's obligations and your personal finances.

It's possible to get a business credit card without a personal guarantee, but it's often more challenging. These cards usually require a higher level of financial stability and a strong business credit score. Luckily, some credit card issuers offer alternative routes to getting approved. Ramp explains how personal guarantees work and what to look for when deciding on a no-personal-guarantee business credit card.

What is a personal guarantee on a business credit card?

A personal guarantee on a business credit card is a legally binding agreement that makes you personally responsible for repaying any unpaid balances if your business can't. This means you're on the hook for the debt if your company can't pay.

With a personal guarantee, card issuers can pursue your individual assets and report negative payment history to personal credit bureaus if your business defaults. Late payments or defaults appear on your personal credit report, which can lower your credit score and affect your ability to get personal loans, mortgages, or other financial products.

You might want to avoid personal guarantees to keep your business and personal finances separate. This separation reduces your personal financial risk, protects your personal assets from business creditors, and keeps clear accounting boundaries between business operations and personal finances.

How personal guarantees work

Personal guarantees activate when certain events occur, such as missed payments, defaulting on the card agreement, or business bankruptcy. Once triggered, the lender can legally pursue you for the outstanding balance, regardless of your business structure.

This gives creditors access to your personal finances. They can pursue your personal bank accounts, investments, real estate, and other assets to recover their money. The default also appears on your personal credit report, potentially damaging your credit score for years.

There are two types of personal guarantees—limited and unlimited:

- Limited personal guarantee: A limited guarantee means you're liable for a portion of your business's debt, usually a set dollar amount or percentage.

- Unlimited personal guarantee: An unlimited guarantee means you're responsible for repaying your business's debt in full, including any interest and fees.

A personal guarantee is often necessary to get the funds you need and build your business credit, especially when you're just starting out, but it's important to recognize the risks.

When are personal guarantees required for a business credit card?

Personal guarantees are usually required for small businesses, startups, and companies with limited credit history. Card issuers see these businesses as higher risk because they lack a proven financial track record. Without substantial business assets or steady revenue, issuers want extra security through personal guarantees.

Several factors play into whether a guarantee is required:

- Industry: Businesses in volatile industries often face stricter requirements than those in stable sectors.

- Business structure: Sole proprietorships and partnerships almost always require guarantees, while established corporations with significant revenue may qualify for cards without them.

- Business revenue and maturity: Annual revenue thresholds (often $1 million or more) and time in business (typically two or more years) are common benchmarks for waiving guarantee requirements.

To avoid unexpected personal liability, review the card terms carefully and confirm the guarantee requirements with the issuer before applying for a business credit card.

Who can get a business credit card with no personal guarantee?

Getting a business credit card without a personal guarantee isn’t as simple as filling out an application online. Because issuers shift the risk from you personally to your company, they dig deeper into your business metrics. To get a business credit card with no personal guarantee, you generally need to meet four broad criteria:

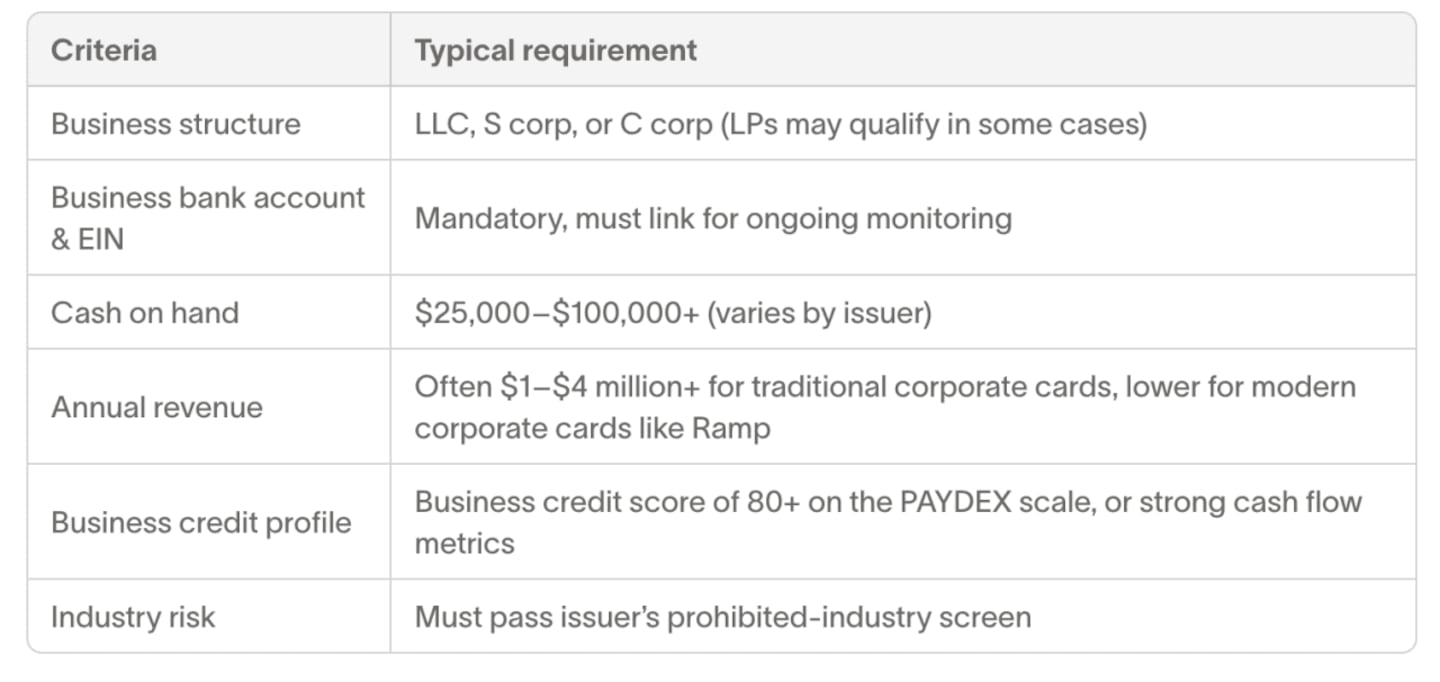

- Incorporated entity with an EIN: LLCs, S corps, C corps, and occasionally LPs with a registered employer identification number (EIN) make up the shortlist of who can qualify.

- Healthy cash balances or revenue: Instead of pulling your personal credit, issuers look at factors like your business bank account balance and annual revenue to determine whether you qualify.

- Established business credit: Because there's no personal backstop, you'll typically need a PAYDEX score near 80 or a clean Experian Intelliscore, but strong cash flow metrics can substitute for a thinner credit report.

- Low-risk credit profile: Businesses in high-risk industries will have a harder time getting approved for a no-personal-guarantee business credit card, typically requiring additional documentation, if not outright rejection.

If your business is incorporated, has a healthy cash balance, and can prove reliable cash flow, you’re in a good position to qualify for a business credit card without a personal guarantee. New business owners or entrepreneurs with little revenue will likely need to build a while longer or accept the risk of a personally guaranteed card first.

Qualification requirements at a glance

Ramp

Key benefits of no personal guarantee business credit cards

Business credit cards without a personal guarantee offer major advantages for business owners who want a true separation between business and personal finances. These cards provide structural protections that standard business credit cards can't match:

- No personal liability: Your personal finances are protected if your business faces financial trouble. Defaults, late payments, or collections stay on your business credit profile and never appear on your personal credit report. This keeps your personal credit score safe, even during business challenges.

- Higher credit limits: Approval is based on your business's financial strength, revenue history, and performance—not your personal credit score. That means even startups and small businesses could get access to a high-limit business credit card as long as they meet the card's requirements.

- Additional business benefits: Many cards offer advanced expense tracking tools to help track spending and simplify tax prep. They may also offer partner perks like discounts on software, shipping, or travel that directly impact your bottom line.

What to look for in a no-personal-guarantee business credit card

Choosing the right no-personal-guarantee business credit card means looking beyond the simple absence of a guarantee. A systematic approach helps you find the card that best supports your business operations and goals.

Rewards structure

Does the card's rewards program match your main business expense categories? Look at your expense reports from the past year to identify your highest-volume categories. Some businesses benefit more from flat-rate rewards, while others get more value from category-specific bonuses. Still other businesses prefer cashback to points-based rewards.

Credit limit flexibility

Are the limits high enough for your monthly expenses? Compare them to your typical monthly expenses and anticipated large purchases. Some issuers offer dynamic limits that grow with your business, while others set fixed ceilings. Check if the card allows temporary limit increases for seasonal spikes or major purchases.

Fee transparency

Fee structures matter, too. Weigh annual fees against the rewards and benefits. Foreign transaction fees are important if you work with international vendors or travel. Ideally, pay your balance in full each month, but know the APR in case you need to carry a balance.

Additional business finance features

Additional expense management and accounting features can add significant value:

- Automated expense management systems help you monitor and report on business spending.

- Customizable spending controls for employees, departments, or vendors can help you control business expenses and enforce your expense policy.

- Integrations with your accounting software or enterprise resource planning (ERP) system reduce manual reconciliation work.

- Other partner perks like airport lounge access, shipping discounts, or software subscriptions, depending on your needs and spending habits.

Qualification requirements

Are you likely to meet the card issuer's criteria for approval? Make sure you understand the requirements before applying, and collect any documents or other information you’ll need to provide with your application to ensure the process goes smoothly.

This story was produced by Ramp and reviewed and distributed by Stacker.

Sign Up

Sign Up